Anyone following prices in the Swedish energy market over the past year will have noticed a clear downward trend in ancillary services markets. Prices on FCR and mFRR are now substantially lower than the levels seen during 2022–2024. What is driving these developments? Are lower prices here to stay? And how should market participants navigate the changing market environment?

/https%3A%2F%2Fwww.flower.se%2Fwp-content%2Fuploads%2F2026%2F05%2FELLEVIO.Final-113_webedit.jpg)

Not long ago, battery energy storage systems (BESS) represented an extremely lucrative opportunity in Sweden. Battery systems were still a relatively new technology, competition across ancillary services markets was low, and prices were high. The period was often described as a “BESS gold rush”, as even small-scale asset owners could generate returns that quickly exceeded their initial capital investment.

In 2024, however, the first signs of market saturation began to emerge as the FCR-D market started to soften. For many market participants, this had a significant negative impact, as business models were often built around the historically high price levels in the FCR markets. Yet this market correction was ultimately not a question of if, but when, as capacity supply had been growing at a pace that increasingly pointed toward saturation.

Today, ancillary services markets are once again experiencing downward pressure. This time, the mFRR CM market is the main driver of the trend, following a period in which it has served as the primary revenue source for BESS owners for much of the past year.

Compared to March last year, prices for both mFRR CM up and down are now lower in all Sweden’s bidding zones. Within March itself, mFRR CM Up declined in SE1–SE3 compared with February but increased slightly in SE4, while mFRR CM Down increased in SE1 and SE2. Lower spot prices in March also contributed to lower clearing prices, since resources such as hydropower and thermal power could bid capacity at lower prices when their opportunity costs declined.

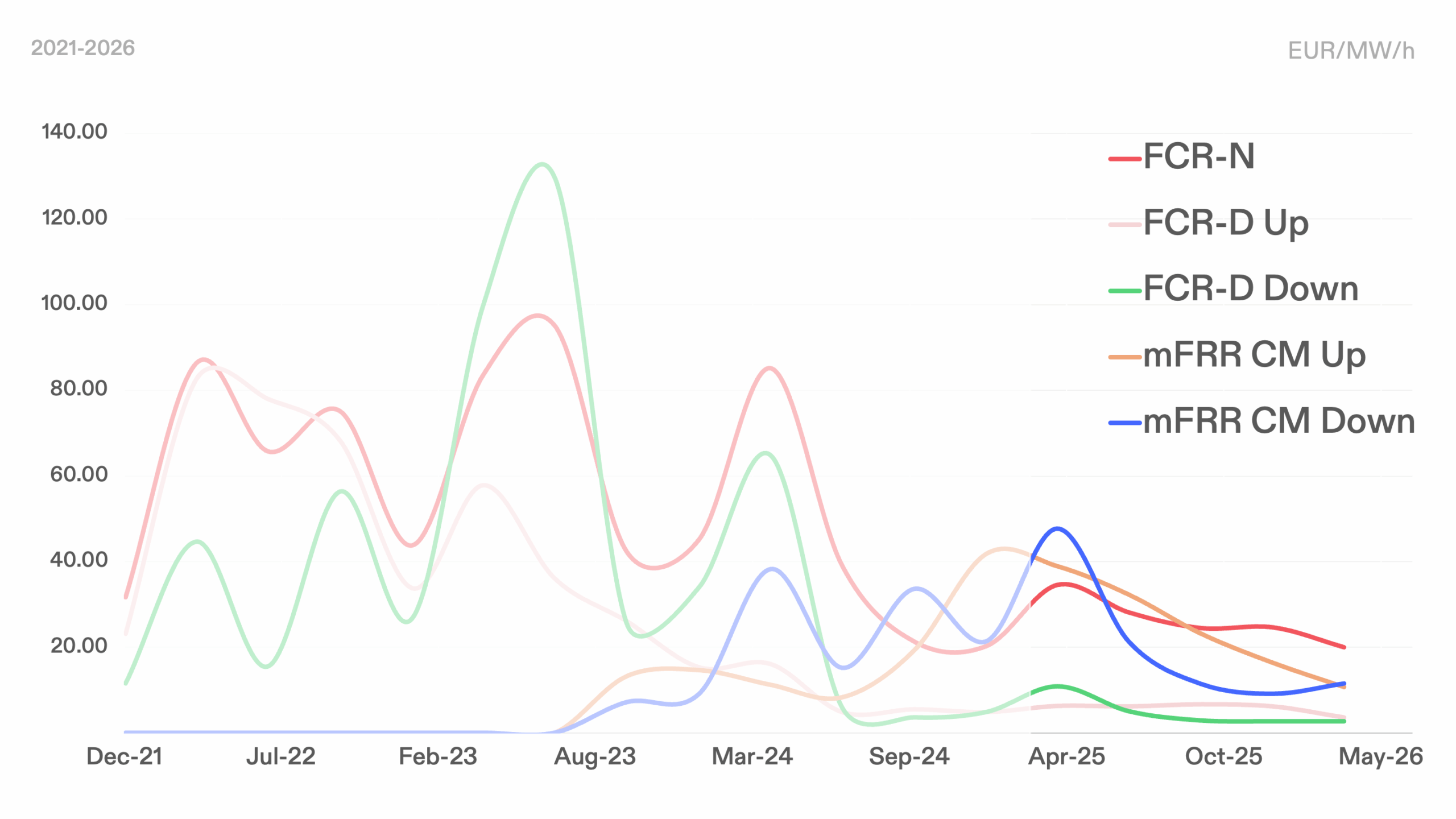

In Sweden, average prices on ancillary service markets have gradually stabilized over the years.

The FCR picture is somewhat more mixed. FCR-N and FCR-D Up decreased compared to February and landed slightly below March levels from the previous year. FCR-D Down, however, moved in the opposite direction and remained in line with March last year. FCR is a more mature market, and following the price decline several years ago, prices have largely stabilized at lower levels.

1. Supply is growing faster than demand

The single most important explanation of the downward trend on ancillary service markets is the dramatic increase of prequalified capacity.

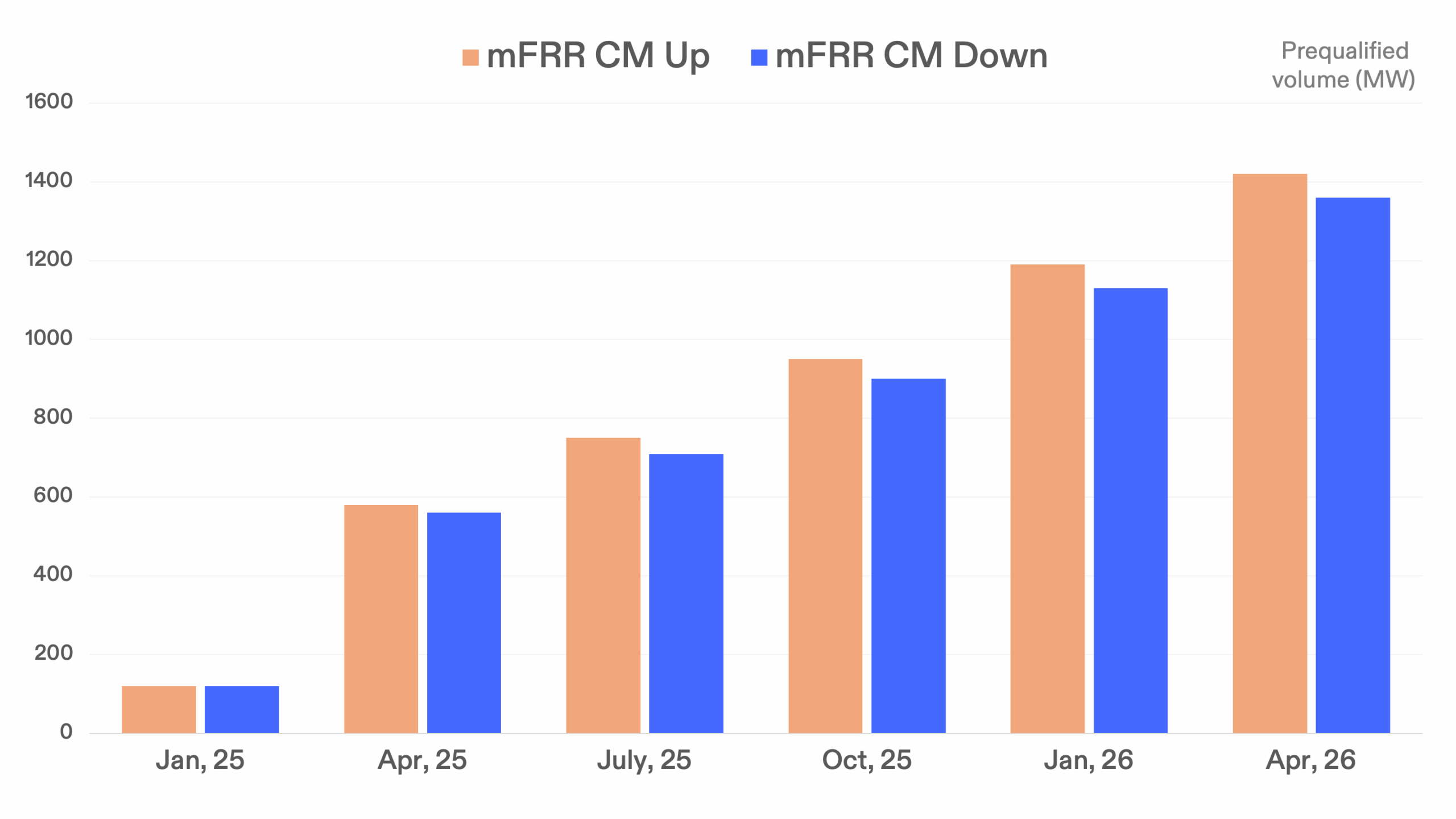

The Swedish TSO Svenska kraftnät’s own data illustrates this clearly. Between January and April 2026, prequalified BESS capacity on mFRR increased by 230 MW — a 20% increase in just one quarter. Beyond BESS volumes, prequalified mFRR capacity for wind power increased during the same period by nearly 30% for upward regulation and just over 20% for downward regulation. Thermal power capacity in mFRR also grew by as much as 46% and now amounts to nearly 700 MW. Altogether, the total prequalified supply in mFRR is now larger than ever before, dominated by resources that can offer capacity at very low prices.

Prequalified BESS volume has increased substantially on the mFRR capacity markets in Sweden from 2025 to 2026.

At the same time, the Svenska kraftnät’s procured volumes have not grown at the same pace. Batteries, wind power, and other flexible resources with low opportunity costs are therefore now competing for the same procured volumes as they did a few years ago.

2. Seasonality and reduced system stress

The recent price developments can also be linked to broader system dynamics. In March, hydropower production declined compared with both February and March last year, while wind power production increased and exceeded levels from the previous year. This reflects a typical spring pattern characterized by stronger winds, lower electricity demand, and hydropower reservoirs being replenished ahead of the spring flood season. Higher wind generation also contributes directly to downward pressure on FCR and mFRR prices, as wind power can provide these services at very low cost.

The high prices seen during 2022–2024 were not a normal state of the market. They were the result of a combination of the energy crisis, market uncertainty, and a maturity premium for early movers. While today’s prices are not expected to continue on a sharp decline, a new pricing normal is now being established. BESS owners should therefore expect earnings that follow the realities of a new stabilized market.

Both today and in the near future, profitability will increasingly depend on the ability to optimize across multiple markets and time horizons. For existing assets, the focus is on the factors that can actually be influenced: access to the right markets, well-developed trading strategies, optimization with grid fees in mind, and maximizing asset availability.

The center of gravity is gradually shifting from capacity-based revenues toward more continuous energy trading. Actively allocating the right volume to the right market at the right time, while combining ancillary services with continuous participation in the energy markets, is becoming an increasingly important part of how batteries create value.

Today, this largely revolves around the interaction between mFRR EAM and intraday trading. At the same time, the gradual rollout of PICASSO across the Nordics may over time broaden participation in aFRR markets and create additional opportunities for flexible assets.

For Flower, the focus lies in continuously strengthening its optimization capabilities across ancillary services and energy markets. Simlutaneously, Flower is adapting its trading strategies to evolving market dynamics and new market structures. As the Nordic market leader in battery trading and optimization, Flower continues to support asset owners in navigating an increasingly competitive and rapidly changing market environment.

For more, get in touch.

/https%3A%2F%2Fwww.flower.se%2Fwp-content%2Fuploads%2F2025%2F11%2FDJI_0638_Bredhalla_TomasArlemo_1440x9601.jpg)

/https%3A%2F%2Fwww.flower.se%2Fwp-content%2Fuploads%2F2025%2F06%2FHanhals-15-MW-Ellevio-1000x1246-1.png)

/https%3A%2F%2Fwww.flower.se%2Fwp-content%2Fuploads%2F2025%2F02%2FELLEVIO.Final-102_web-1000x1246-1.jpg)

/https%3A%2F%2Fwww.flower.se%2Fwp-content%2Fuploads%2F2024%2F10%2FSkoldinge-BESS.jpg)